for Personal Loan: A Comprehensive Guide" width="688" height="456" />

for Personal Loan: A Comprehensive Guide" width="688" height="456" />for Personal Loan: A Comprehensive Guide" width="688" height="456" />

Promissory notes serve as binding legal agreements between lenders and borrowers, making them an ideal vehicle to lend money for personal reasons.

With a promissory note, the terms of the loan are documented, which means that both parties know exactly what to expect when it comes to repayment, interest, and any other concerns that may arise.

Before you use a promissory note for a personal loan, make sure you understand the potential legal implications and how the loan may impact you.

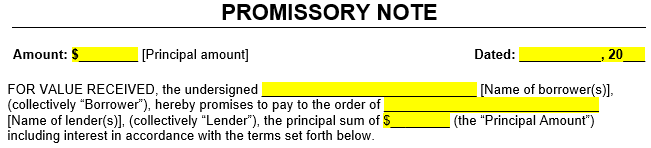

A promissory note is a legal document that lays out the terms of a loan. It formalizes a borrower’s promise to repay a loan and the conditions under which the borrower makes or must issue that repayment.

With a promissory note in hand, both borrower and lender know exactly what to expect from the process, which means that repayment will often go much more smoothly.

Promissory notes are pivotal in personal loan agreements. They detail the terms of a loan so that neither party has any questions about it, including the repayment schedule and terms.

Furthermore, a promissory note secures the lender’s interests by legalizing the terms of the loan. It may spell out specific consequences if the buyer defaults on the loan or any collateral used to secure the loan .

Having a promissory note also protects both parties’ legal interests as they move forward with the loan process. While the lender can seek legal assistance if the borrower fails to pay back the funds promptly, the borrower can insist that the lender adhere to the terms of the promissory note, including not seeking repayment before the time laid out in the document.

Suppose, for example, that you have a friend or family member who needs a personal loan to help during a hard time. You might choose to issue a personal loan at a lower interest rate than the bank.

Using a promissory note not only offers you legal recourse if your friend or family member does not pay, but it also lays out more specific terms than a handshake agreement, which means that both of you have a better idea of when the loan will be taken care of.

for Personal Loan" width="710" height="405" />

for Personal Loan" width="710" height="405" />

When writing a comprehensive and legally binding promissory note for personal loans, make sure you are clear and specific in all of your terms and conditions. You want to create a document that lays out expectations on both sides and provides protection to both the borrower and lender.

Any time you want to craft a legal contract, it’s important to ensure that the document contains all the essential details. By laying out all the information in the contract, you ensure that there are no loopholes that could cause problems later.

Spell out all relevant details, and do not leave anything out, including:

If there are questions, hash them out before you sign the contract, and include the answers in writing.

A negotiable promissory note can be transferred or sold to another party. The other party can use the promissory note much like they would cash or any other investment, and they can transfer it at any time.

In the case of a personal loan between two parties, on the other hand, promissory notes are often non-negotiable: that is, they cannot be transferred, and only the party named in the document has the right to collect on the loan.

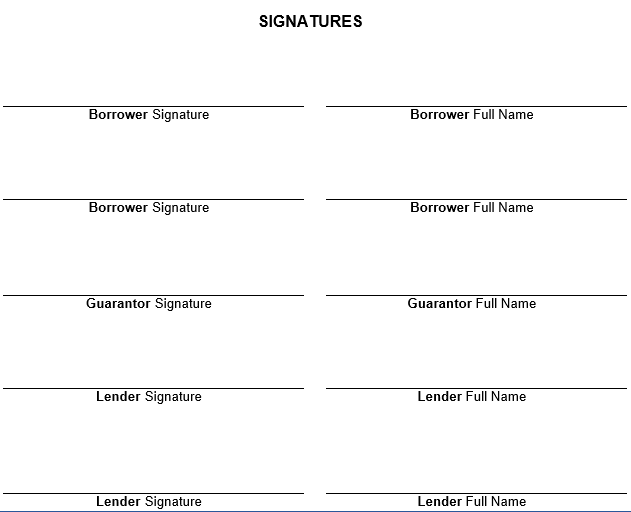

To legalize a promissory note, you should have signatures from both borrower and lender. In cases where more than one party will bear responsibility for the loan, make sure to include both signatures.

A promissory note will contain several essential features.

Those elements clearly stated can protect both the borrower and the lender in case of a potential dispute.

If the borrower defaults on the loan, lenders may have legal options for seeking reimbursement . First, they should submit a request directly to the borrower. After that, they may turn to a collections agency or file a lawsuit to recover the funds specified in the document.

If the loan was secured, the lender may also have the right to seize the property put up as collateral if the borrower defaults. Clear documentation of the loan and its terms can make it much easier to collect since the courts consider the promissory note a legally binding document.

In a negotiable promissory note, the lender has the right to transfer, or assign, the right to collect on the loan to a third party. Transferring the loan would absolve the initial lender of the need to collect on the loan, shifting that right to another party.

A lender might, for example, choose to sell the note to a third party to collect the funds from the loan earlier than anticipated. Selling the loan would provide them with the funds they need immediately.

The borrower would then pay the new holder of the promissory note. In the case of a promissory note with payment on demand, selling the note could result in the note being called due earlier than anticipated.

In the case of a note with a set repayment schedule or date, however, the new holder of the note would need to hold to the initial terms of the loan.

A promissory note is typically a contractual agreement between two parties – a borrower and a lender. The lender will provide the borrower with the amount listed in the promissory note and collect on the note at the predetermined time.

The borrower promises to repay the lender based on the terms of the promissory note. That may include payments over time, or it may mean that the borrower is responsible for repaying the full amount of the loan at a time named by the lender.

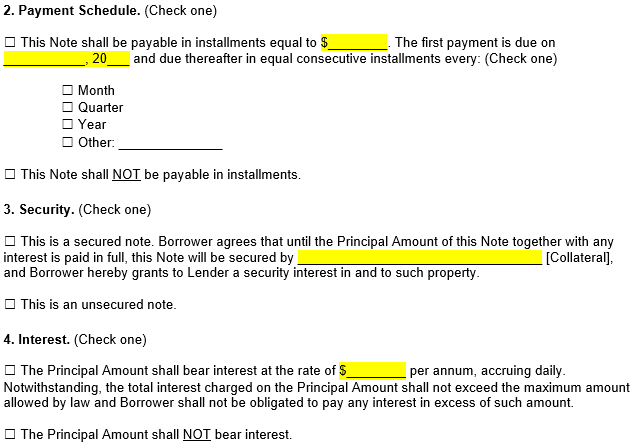

There are several ways to structure interest rates and payments for a personal loan. The promissory note should lay out expectations for repayment so that both parties will understand what is expected of them.

Setting interest rates is often complicated. While the banks may have an average interest rate they assign for personal loans, a private loan may have interest rates determined by the borrower and lender.

Fixed interest rates are set at the time the loan is issued and remain the same for the duration of the loan. Variable interest rates, on the other hand, are changed or revisited at predetermined times throughout the loan’s lifetime and are often based on current market norms.

Variable interest rates often start lower than fixed rates but have the risk of increasing more than anticipated.

There are several strategies used to determine repayment terms. The one you choose may depend on the duration of the loan , payment amount, or even on the party to whom you are issuing the loan.

Accrued interest is determined by multiplying the loan’s outstanding balance by the interest rate and compounding it daily or monthly, thus increasing the total debt. This interest is added to the loan’s principal, raising the amount due.

By carefully considering the legal requirements for signing and the best practices for storage, lenders and borrowers can safeguard the enforceability and accessibility of promissory notes.

Witness Requirements – The necessity for witnesses or notarization can vary depending on the jurisdiction. While not all states require a witness or notary for a promissory note to be enforceable, having a notarized document can add a layer of verification and legal validity.

State-Specific Requirements – Some states may have specific requirements regarding the execution of promissory notes, such as the need for certain disclosures to be included within the note or specific wording. It is important to consult legal advice to ensure compliance with local laws.

Physical Storage – Keep the original signed document in a secure, fireproof, and waterproof location, such as a safe or safety deposit box. Ensure that both parties have copies of the signed note, but the original should be kept with the lender or in a mutually agreed-upon secure location.

Digital Storage – Scanning and storing a digital copy of the note can be a practical step for backup. Use encrypted digital storage solutions to protect the document from unauthorized access. Cloud storage services offer convenient access but ensure they comply with security standards and provide adequate privacy protections.

Access – Whether stored physically or digitally, the storage method should ensure that authorized parties can access the document when needed without compromising security. Establish clear procedures for retrieving the note, especially if stored in a safety deposit box or through a digital platform that requires password access.

Enforceability – The content of the note, such as the amount borrowed, interest rate, repayment schedule, and any collateral, should be clearly stated. Regular updates or amendments to the note should be signed and stored following the same protocols as the original.

The consequences of defaulting on a loan laid out by a promissory note can, in many cases, be the same as when a borrower defaults on any other type of loan. The lender may decide to:

If the lender does take the loan to collections or file a lawsuit, it can have a significant impact on the borrower, including a decrease in their credit score. The borrower may also face financial repercussions for failing to repay the loan, including wage garnishment .

Note, however, that there can also be financial consequences for the lender when the borrower defaults on a loan. The lender may have to pay the collection agency for their services or allow the collection agency to purchase the promissory note at a discount, which means they may not be able to collect the full amount of the loan.

If the lender chooses to file a lawsuit, they may have to pay for the cost of a lawyer or the cost of court filing fees, which may ultimately lead to unanticipated, higher costs.

If you choose not to move forward with a promissory note, there are other strategies you can use to secure a personal loan. You might, for example, choose to use a simpler loan agreement , which might contain fewer terms or lack the ability to transfer it to another party.

Others may choose to provide collateral, which the lender would hold until the borrower returns the loan amount . While these strategies may prove beneficial, a promissory note offers a higher overall degree of legal protection.

The terms laid out in a promissory note protect both the borrower and the lender, ensuring that their financial futures remain as secure as possible and increasing the odds that both sides will adhere to the terms of the loan.

Laying out those legal terms, from the payment schedule to the date it comes due, is essential for protecting both parties. Before you sign a promissory note as either a borrower or lender, make sure you have a strong understanding of the terms and what they will mean for you.

Legal Content Editor

Yassin Qanbar is an SEO Content Editor at LegalTemplates, passionate about translating complex legal concepts into helpful, user-friendly information.

Need to draft a promissory note? Check out our templates